|

Help | | | News | | | Credits | | | Search | | | Guestbook | | | Forum | | | Shop | | | Contact Us | | | Welcome |

Westwood Works 1903-2003 |

|||||||||||||||||

To try to make all who work at Baker Perkins feel part of the same enterprise: to create a greater interest in their work by giving employees the opportunity to participate in the profits of the Company in the years of real prosperity and to continue and extend the spirit of co-partnership which has existed in the past.

The scheme was introduced in 1947 and was based on a formula related to the Company's profits. All full time permanent employees of Baker Perkins Ltd over the age of 21 participated after completion of two years' service.

In 1947, a total of £40,689 (see below) was shared between qualifying employees which meant that each received quite a significant sum. Many local shops stocked up in anticipation of the yearly pay-out.

The profit sharing pool calculated from the Company profit was distributed to eligible employees pro rata to both individual earnings and length of service category. Those with over 10 years service received a 100% profit share, those with 6 to 10 years service a 75% share and those with 2 to 6 years a 50% share.

Profit shares were paid in cash after the deduction of PAYE.

At the time of the introduction of the scheme, the company was a Public Company but was not listed on the Stock Exchange, London. In later years, probably after the Company's shares were quoted in 1957, in order to conserve cash, profit shares after tax were settled by the allocation of ordinary Shares in the Company. A mechanism was provided for those who wished to continue to receive cash, their shares being sold on their behalf.

In 1964, when the group was reorganised (see The Holdings Building), the profit sharing scheme was extended to the UK Group. It was not, however, feasible to include employees of non-UK Group Companies.

A major change in the UK pension scheme was undertaken in the 1970s, with the alteration of the benefits from an average salary formula to one based on final salary. The additional funding this required from the Company could only be met if the Employee Profit Sharing Scheme was discontinued.

There was some dissatisfaction with the Board's decision, particularly from younger employees, but clearly, there were advantages in the enhancement of pension benefit which most people recognised.

|

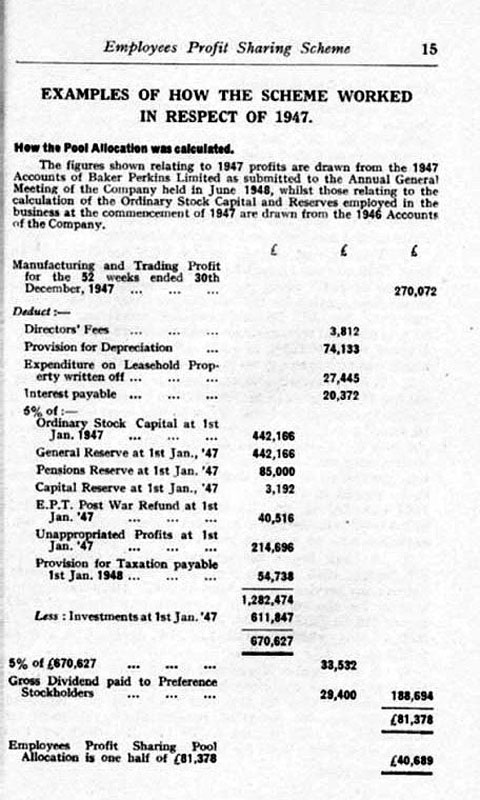

This extract from the 1947 accounts was used to show employees how the Scheme would work and how the amount to be distributed would be calculated. It will be seen that the sum to be shared between employees was half of the Company's net profit after allowing a basic return on the capital employed in the business. |

All content © the Website Authors unless stated otherwise.